The Medicare Surcharge Trap: How Higher Income Can Lead to Higher Medicare Premiums

Many retirees spend years carefully planning for taxes, Social Security, investment withdrawals, and healthcare costs. Yet one retirement expense often catches people completely by surprise.

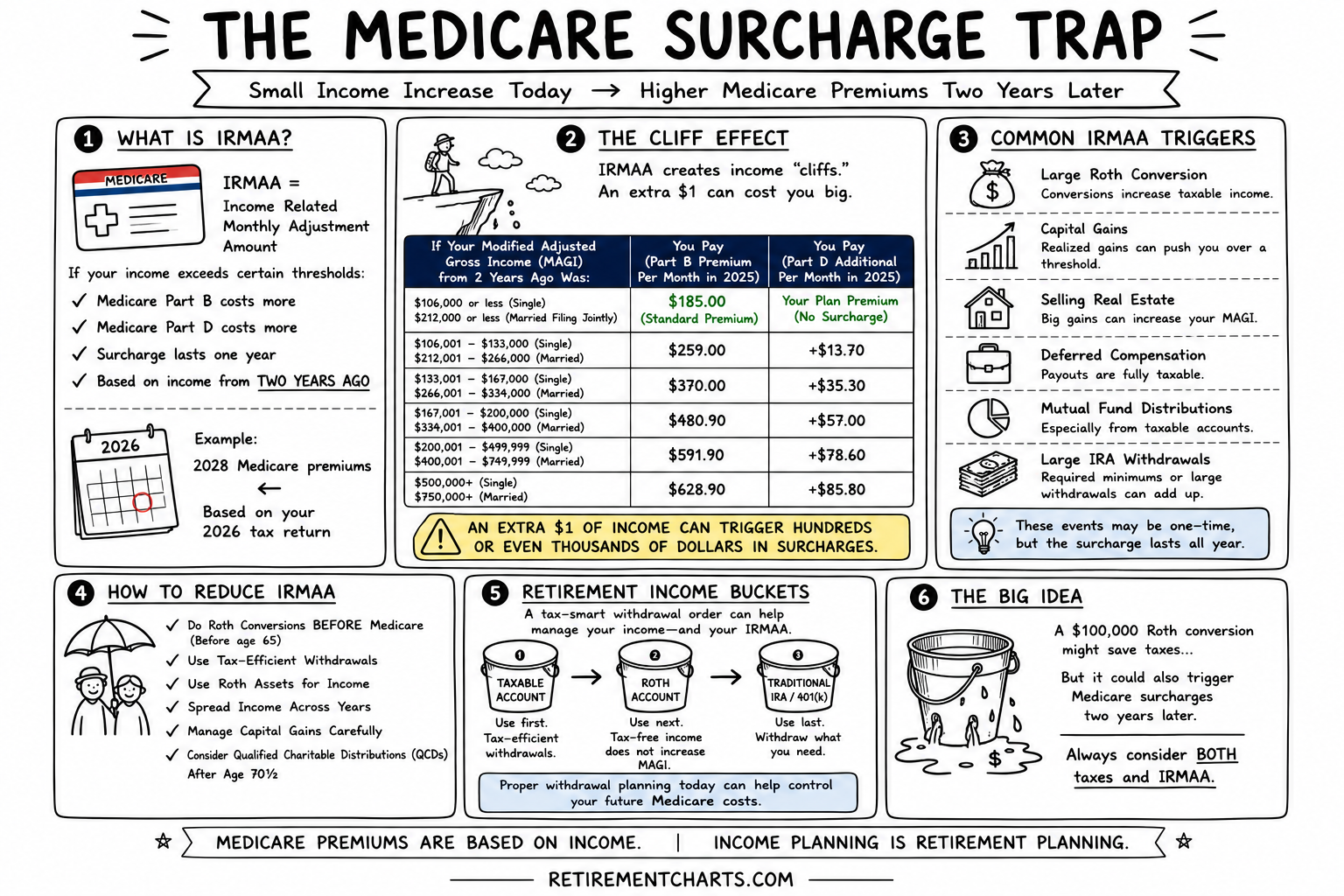

It is called IRMAA, which stands for Income Related Monthly Adjustment Amount.

Most retirees simply know it as the Medicare surcharge.

The frustrating part is that many people do not discover IRMAA until after the damage has already been done. A large Roth conversion, a substantial capital gain, the sale of a property, or a large IRA withdrawal can trigger higher Medicare premiums years later.

The result is an unpleasant surprise in the form of a higher monthly Medicare bill.

Understanding how IRMAA works can help retirees avoid unnecessary costs and make more informed decisions about their retirement income strategy.

What Is IRMAA?

IRMAA is a surcharge added to Medicare Part B and Medicare Part D premiums for higher-income retirees.

Medicare is designed so that most beneficiaries pay a standard premium. However, individuals with income above certain thresholds pay additional amounts on top of those standard premiums.

The government determines whether you owe IRMAA by looking at your Modified Adjusted Gross Income, often referred to as MAGI.

The important detail that many people overlook is that Medicare does not use your current year's income.

Instead, Medicare typically looks at your tax return from two years ago.

For example, your Medicare premiums in 2028 will generally be based on your 2026 tax return.

This creates a delayed effect that often catches retirees off guard.

Someone might complete a large Roth conversion in 2026, feel great about the tax planning decision, and then wonder in 2028 why their Medicare premiums suddenly increased.

The answer is often IRMAA.

Why IRMAA Feels Like a Trap

One of the most frustrating aspects of IRMAA is that it creates income cliffs.

As your income crosses certain thresholds, Medicare premiums can jump significantly.

In some cases, an extra dollar of income can move you into the next IRMAA bracket and trigger hundreds or even thousands of dollars of additional healthcare costs.

Imagine a retiree whose income falls just below an IRMAA threshold.

Everything is fine.

Now imagine that same retiree realizes a small capital gain, receives a larger than expected mutual fund distribution, or completes a slightly larger Roth conversion.

That additional income may push them into the next bracket.

The result is not just additional taxes. It may also mean higher Medicare premiums for an entire year.

This is why many financial planners pay close attention to income levels near IRMAA thresholds.

The goal is not necessarily to avoid income altogether. The goal is to understand the consequences before making a decision.

Common Events That Trigger IRMAA

Many retirees assume IRMAA only affects extremely wealthy households.

That is not necessarily true.

Several common financial transactions can push retirees into higher Medicare premium brackets.

One of the most common triggers is a Roth conversion.

Roth conversions can be powerful planning tools. They can reduce future Required Minimum Distributions, create tax-free assets for retirement, and potentially benefit heirs.

However, the amount converted is generally treated as taxable income in the year of the conversion.

A large conversion may increase taxes and trigger IRMAA.

Capital gains are another common culprit.

Selling appreciated investments in a taxable account can create significant gains that increase your MAGI.

The sale of real estate can have a similar effect.

Many retirees are surprised to discover that selling a vacation property, rental property, or other highly appreciated asset can impact future Medicare premiums.

Large IRA withdrawals can also create problems.

Some retirees need additional income for a major purchase or unexpected expense. Others are forced to take larger withdrawals because of Required Minimum Distributions.

Regardless of the reason, higher taxable income can lead to higher Medicare costs.

Even mutual fund distributions can contribute to the problem.

Retirees who own actively managed mutual funds in taxable accounts may receive capital gain distributions even if they never sell a single share.

How Much Can IRMAA Cost?

The exact amount changes periodically as Medicare updates premiums and income thresholds.

What matters most is understanding the concept.

Higher income can lead to significantly higher Medicare Part B premiums and additional Part D surcharges.

For some retirees, the additional cost may be relatively modest.

For others, especially married couples who remain in higher brackets for multiple years, the cumulative impact can be substantial.

Over the course of retirement, unnecessary IRMAA surcharges can cost thousands or even tens of thousands of dollars.

That is real money that could otherwise remain invested or available for spending.

Strategies to Reduce IRMAA

The good news is that IRMAA is often manageable with proper planning.

One of the most effective strategies is completing Roth conversions before Medicare begins.

For many individuals, the years between retirement and age 65 represent a valuable planning window.

Income is often lower during this period, creating opportunities to convert portions of traditional retirement accounts without triggering Medicare surcharges.

Managing withdrawals strategically can also help.

Retirees with multiple account types may be able to draw income from taxable accounts, Roth accounts, and traditional retirement accounts in a way that controls annual taxable income.

Roth assets are particularly valuable because qualified withdrawals generally do not increase MAGI.

This can provide flexibility when managing income levels.

Spreading income-producing events across multiple years can also be beneficial.

Rather than realizing a large gain all at once, it may be possible to spread transactions over several years and avoid crossing major thresholds.

Qualified Charitable Distributions, commonly known as QCDs, can be another useful tool.

For retirees over age 70½, QCDs allow charitable gifts directly from an IRA without increasing taxable income in the same way as traditional withdrawals.

In some situations, this can help reduce both taxes and future Medicare surcharges.

The Bigger Picture

It is important not to let IRMAA completely dictate financial decisions.

Sometimes paying the surcharge still makes sense.

For example, a Roth conversion that generates substantial long-term tax savings may still be worth doing even if it triggers IRMAA temporarily.

The key is awareness.

Too many retirees focus exclusively on income taxes while ignoring the impact on Medicare premiums.

Retirement income planning is about understanding all the moving pieces.

Taxes matter.

Social Security matters.

Required Minimum Distributions matter.

And Medicare premiums matter too.

The most successful retirement strategies evaluate all of these factors together.

The Bottom Line

Medicare premiums are not based solely on age. They are also influenced by income.

That is why IRMAA deserves attention from every retiree and pre-retiree.

A large Roth conversion, capital gain, property sale, or IRA withdrawal may have consequences that extend beyond your tax return.

Those decisions can affect your Medicare premiums years later.

The goal is not necessarily to avoid every surcharge. The goal is to avoid surprises.

Understanding how IRMAA works allows you to make more informed decisions about retirement income, taxes, and healthcare costs.

At its core, the lesson is simple.

Medicare premiums are based on income.

Income planning is retirement planning.