The Basics of Wealth Building

Many people believe wealth is built by finding the perfect investment, predicting market movements, or discovering some secret strategy that others have overlooked. The reality is far less exciting, but much more encouraging.

Most wealth is built through a handful of simple habits practiced consistently over long periods of time.

The good news is that these habits are available to almost everyone.

You do not need insider information. You do not need to be a financial expert. You do not need to spend your evenings studying stock charts or watching financial news.

You simply need to understand the basic building blocks of wealth and give them time to work.

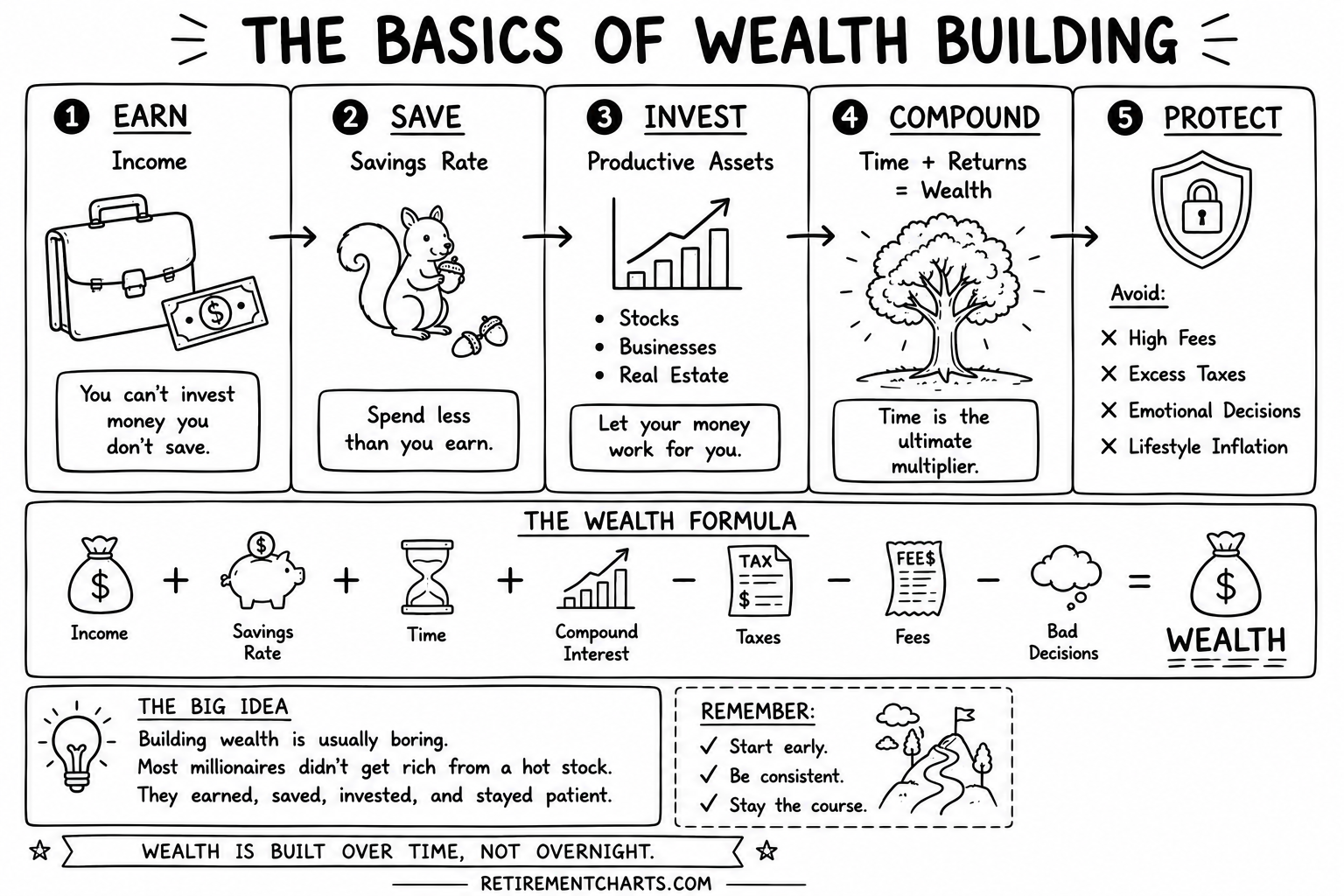

The chart above outlines what I consider the five pillars of wealth building: earn, save, invest, compound, and protect. Together, these principles form the foundation of nearly every successful financial journey.

Step One: Earn

Every wealth-building journey begins with income.

Whether you earn money through employment, self-employment, a business, or another source, income is the fuel that powers everything else.

Many people spend enormous amounts of time trying to optimize their investments while paying very little attention to increasing their earning potential. Early in life, your ability to generate income is often your most valuable financial asset.

This does not mean everyone needs to chase the highest-paying career. It simply means recognizing that income creates options.

The more income you generate, the more flexibility you have to save, invest, and build long-term wealth.

The first step in wealth building is simple: create value, earn income, and maintain a focus on growing your earning power over time.

Step Two: Save

Income alone does not create wealth.

Many high earners struggle financially because they spend everything they make. Meanwhile, many households with moderate incomes quietly build substantial wealth through consistent saving.

Saving is the bridge between earning money and building wealth.

Every dollar that is spent today is a dollar that cannot be invested for tomorrow.

This is why savings rate is often more important than investment selection, especially during the early stages of wealth building.

A person earning $75,000 per year and saving 20 percent of their income is often in a better position than someone earning $150,000 but saving almost nothing.

The goal is not extreme frugality. The goal is creating a gap between what you earn and what you spend.

That gap becomes your future wealth.

One of the most powerful financial habits is simply learning to live slightly below your means. Over time, that difference compounds into something much larger.

Step Three: Invest

Saving money is important, but saving alone is rarely enough.

Cash sitting in a bank account generally struggles to keep pace with inflation over long periods of time. To build substantial wealth, your money must begin working for you.

This is where investing enters the picture.

Investing allows you to participate in the growth of productive assets.

Historically, some of the most effective wealth-building assets have included businesses, stocks, and real estate. These assets produce income, profits, and growth over time.

The key is understanding that investing is not about getting rich quickly.

It is about owning productive assets and allowing those assets to create value year after year.

Many investors make the mistake of chasing whatever investment is currently popular. They move from one trend to another hoping to find the next big winner.

Successful investors often take the opposite approach.

They build diversified portfolios, keep costs low, remain patient, and focus on long-term ownership rather than short-term speculation.

Investing is not about excitement.

It is about discipline.

Step Four: Compound

This is where the magic happens.

Compound interest is one of the most powerful forces in finance because it allows your money to earn returns, and then allows those returns to earn returns as well.

In the early years, the effects can seem small.

An account grows gradually.

Progress feels slow.

Many people become discouraged because the results do not appear dramatic.

Then something interesting happens.

Over time, the growth begins to accelerate.

The earnings generated by the portfolio become larger than the contributions being made.

Eventually, the portfolio begins producing meaningful growth almost on its own.

This is why time is such an important ingredient in wealth building.

A great investment strategy applied for five years can produce good results.

The same strategy applied consistently for thirty or forty years can produce life-changing results.

Compound growth rewards patience.

It rewards consistency.

Most importantly, it rewards time.

The earlier you begin, the more powerful compounding becomes.

Step Five: Protect

Building wealth is important.

Keeping it is equally important.

Many investors spend decades accumulating assets only to undermine their progress through avoidable mistakes.

This is where protection comes into play.

The chart highlights four common threats to long-term wealth.

The first is high fees.

Every dollar paid in unnecessary investment expenses is a dollar that cannot compound for your future. Over decades, even seemingly small fees can have a significant impact on portfolio values.

The second threat is excess taxes.

Taxes are a reality of investing, but thoughtful planning can often reduce unnecessary tax drag and allow more of your money to remain invested.

The third threat is emotional decision-making.

Fear and greed have probably destroyed more wealth than market declines ever have.

Investors frequently buy after markets rise and sell after markets fall. Unfortunately, that behavior often leads to poor long-term results.

The final threat is lifestyle inflation.

As income rises, spending tends to rise as well. There is nothing wrong with enjoying the fruits of your labor, but continually increasing spending can make it difficult to build meaningful wealth.

Protecting wealth requires discipline, perspective, and a long-term mindset.

The Wealth Formula

The chart summarizes wealth building with a simple formula:

Income

Plus savings rate.

Plus time.

Plus compound interest.

Minus taxes.

Minus fees.

Minus bad decisions.

Equals wealth.

Notice what is missing from the formula.

There is no mention of predicting the market.

There is no mention of finding the next hot stock.

There is no mention of complex strategies or financial engineering.

The formula is remarkably simple.

That simplicity is what makes it powerful.

The Big Idea

Perhaps the most important lesson from this chart is that building wealth is usually boring.

Most millionaires did not become wealthy through luck.

They did not discover a secret investment.

They did not consistently outsmart the market.

Instead, they followed a process.

They earned income.

They saved consistently.

They invested in productive assets.

They allowed compound growth to work over time.

And they avoided the mistakes that derail so many investors.

The path to wealth is rarely exciting.

But it is surprisingly straightforward.

Start early.

Be consistent.

Stay the course.

Wealth is built over time, not overnight.